A comprehensive breakdown of e-commerce cybersecurity laws in 2025, outlining the compliance requirements online businesses must meet to protect customer data.

E-commerce platforms remain prime targets for cyberattacks, pushing regulators worldwide to tighten security and data protection requirements. In 2025, online businesses face a growing patchwork of cybersecurity laws that set clearer expectations around data handling, breach reporting, and risk management. Understanding these legal obligations is no longer optional as compliance now plays a central role in protecting customer data, avoiding regulatory penalties, and maintaining consumer trust.

E-commerce businesses face an increasingly complex legal landscape as cyber threats evolve and regulations tighten globally. According to YeetCommerce’s 2025 compliance guide:

“staying ahead of regulatory requirements helps mitigate risks, enhance customer trust, and avoid costly penalties.”

With U.S. online retail sales projected to exceed $1.5 trillion in 2025, understanding and implementing proper cybersecurity compliance has become essential for business survival. This comprehensive guide explains the major e-commerce cybersecurity laws, payment security requirements, consumer rights, penalties for non-compliance, and how to build a robust compliance program.

Source: E-Commerce Compliance Guide 2025

Why Cybersecurity Laws Matter for Online Businesses

E-commerce cybersecurity laws exist to protect consumers’ financial data, personal information, and digital transactions. According to IBM’s Cost of a Data Breach Report 2024:

“the average cost of a data breach reached $4.88 million—a 10% increase over last year and the highest total ever.”

For online businesses, secure payment systems aren’t optional—they’re the bedrock of operations.

Non-compliance creates multiple risks:

Financial Penalties: GDPR fines can reach €20 million or 4% of global annual turnover, whichever is higher, while PCI DSS violations can cost between $5,000 and $100,000 monthly until compliance is restored.

Operational Disruption: Payment processors may suspend services for non-compliant merchants, effectively shutting down online sales.

Reputation Damage: According to Infosecurity magazine:

“95% of breaches can be traced back to user mistakes, and customer trust, once lost, is difficult to rebuild.”

Legal Consequences: Data breaches trigger lawsuits from affected customers, regulatory investigations, and potential criminal charges in severe cases.

Competitive Disadvantage: Customers increasingly choose retailers demonstrating strong security practices, making compliance a competitive differentiator.

Source: Cybersecurity Importance for Businesses

Key Global E-Commerce Regulations

United States: CCPA and FTC E-Commerce Rules

California Consumer Privacy Act (CCPA/CPRA): The CCPA, strengthened by the California Privacy Rights Act (CPRA), is America’s strictest state privacy law. It applies to businesses that collect California residents’ personal information and meet revenue or data volume thresholds.

Key requirements include:

- Providing clear notice about data collection practices

- Offering opt-out mechanisms for data sales

- Honoring requests for data access and deletion

- Maintaining reasonable security measures

- Disclosing data sharing with third parties

Penalties reach $2,500 per violation or $7,500 for intentional violations, with private lawsuits possible for data breaches involving encrypted personal information.

FTC Act Section 5: The Federal Trade Commission enforces unfair or deceptive trade practices in e-commerce. FTC rules require businesses to:

- Accurately disclose terms, conditions, and pricing

- Protect customer data with reasonable security measures

- Honor advertised privacy policies

- Provide clear refund and return policies

- Disclose endorsements and affiliate relationships

The FTC has increasingly focused on data security, issuing substantial fines for inadequate protection of customer information.

European Union: GDPR, PSD2, and Digital Services Act

General Data Protection Regulation (GDPR): GDPR remains the gold standard for data privacy, affecting any business collecting or processing EU residents’ personal data regardless of company location.

Critical requirements:

- Obtain clear, informed consent before collecting personal data (no pre-checked boxes)

- Allow data deletion requests as customers can demand erasure of their information

- Appoint a Data Protection Officer (DPO) if processing large-scale personal data

- Implement privacy by design and default

- Report data breaches to authorities within 72 hours

- Conduct Data Protection Impact Assessments for high-risk processing

According to ISMS.online’s compliance analysis:

“GDPR emphasizes data privacy and gives individuals control over their personal data, which complements PCI DSS 4.0’s focus on secure data handling.”

Payment Services Directive 2 (PSD2): PSD2 regulates payment services across the European Economic Area, requiring:

- Strong Customer Authentication (SCA) for most electronic payments

- Secure communication standards between financial entities

- Open banking APIs allowing third-party access to payment accounts

- Enhanced consumer protection for unauthorized transactions

- Liability frameworks for payment disputes

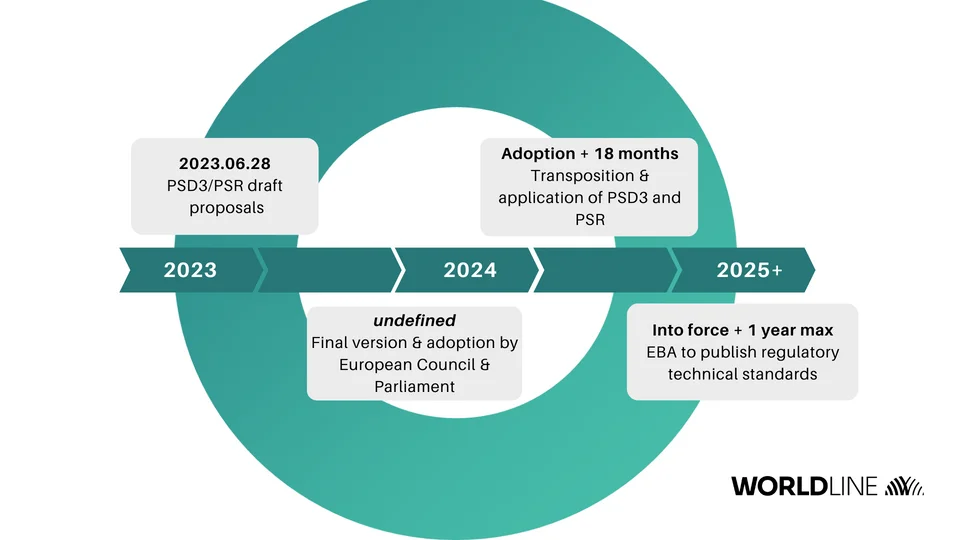

PSD3 is expected:

“to be definitively adopted in 2025, with implementation between 2026 and 2027, further strengthening fraud prevention and expanding scope to instant payments, Buy Now Pay Later, and cryptocurrencies.”

Digital Services Act (DSA): The DSA establishes comprehensive rules for online platforms, including e-commerce marketplaces, requiring:

- Content moderation and illegal content removal

- Transparent advertising and recommendation systems

- User complaint mechanisms

- Cooperation with authorities on illegal activities

- Enhanced due diligence for very large platforms

The EDPB released Guidelines 3/2025 on the complex interplay between the Digital Services Act and GDPR, providing clarity on overlapping requirements.

Source: PSD2 to PSD3 Evolution

United Kingdom: Data Protection Act 2018 and E-commerce Regulations

Post-Brexit, the UK maintains GDPR-equivalent protections through the Data Protection Act 2018, with similar requirements for consent, data subject rights, breach notification, and security measures. Penalties reach £17.5 million or 4% of global annual turnover.

UK E-Commerce Regulations require online businesses to:

- Provide clear business identity and contact information

- Display terms and conditions prominently

- Confirm orders and provide order summaries

- Offer cancellation rights (14-day cooling-off period for distance sales)

- Ensure price transparency including all taxes and delivery charges

The Information Commissioner’s Office (ICO) enforces these requirements, with significant fines for violations.

Asia: Singapore PDPA and India’s DPDP Act 2023

Singapore Personal Data Protection Act (PDPA): Singapore’s PDPA requires organizations to:

- Obtain consent for data collection, use, and disclosure

- Implement reasonable security arrangements

- Notify affected individuals and the Personal Data Protection Commission of breaches

- Appoint Data Protection Officers for certain organizations

- Allow individuals to access and correct their data

Penalties include fines up to SGD 1 million, with the commission increasingly active in enforcement.

India’s Digital Personal Data Protection Act 2023 (DPDP Act): India’s new framework, effective in 2025, establishes comprehensive data protection requirements:

- Clear consent mechanisms for data processing

- Data localization for certain categories

- Rights to access, correction, and erasure

- Breach notification requirements

- Parental consent for children’s data

According to ComplianceHub:

“violations can lead to hefty fines up to INR 250 crores under India’s DPDP Act, making compliance critical for businesses serving Indian customers.”

Payment Security and Data Handling: PCI DSS Requirements

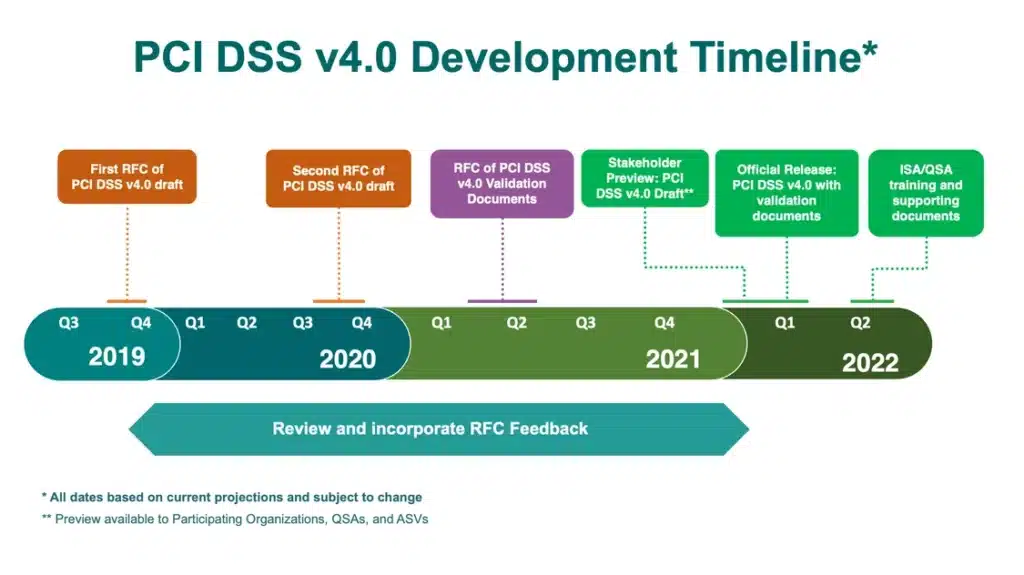

The Payment Card Industry Data Security Standard (PCI DSS) is mandatory for all organizations that store, process, or transmit credit card information. PCI DSS 4.0.1 became effective March 31, 2025, introducing 51 new requirements focused on modern threats.

Source: PCI Compliance Guide

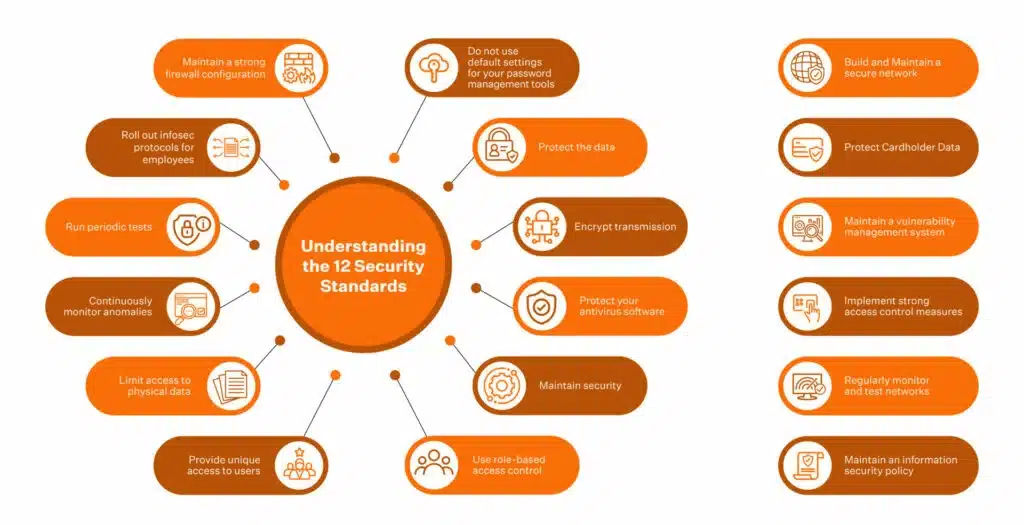

The 12 PCI DSS Requirements

PCI DSS organizes security requirements into six goals with 12 requirements:

Build and Maintain Secure Networks and Systems:

- 1. Install and maintain network security controls (firewalls)

- 2. Apply secure configurations to all system components

Protect Account Data: 3. Protect stored account data with encryption 4. Protect cardholder data transmission with strong cryptography

Maintain Vulnerability Management Program: 5. Protect systems from malware with regularly updated antivirus software 6. Develop and maintain secure systems and software

Implement Strong Access Control Measures: 7. Restrict access to cardholder data by business need-to-know 8. Identify users and authenticate access to system components 9. Restrict physical access to cardholder data

Regularly Monitor and Test Networks: 10. Log and monitor all access to system components and cardholder data 11. Test security systems and processes regularly

Maintain Information Security Policy: 12. Support information security with organizational policies and programs

PCI DSS 4.0.1 New Requirements for E-Commerce

The PCI Security Standards Council released guidance for Requirements 6.4.3 and 11.6.1, which specifically address e-commerce security:

Requirement 6.4.3: Payment page scripts must be managed to prevent unauthorized modification. This requires:

- Inventory of all scripts on payment pages

- Justification for each script’s necessity

- Integrity verification mechanisms

- Change control processes

Requirement 11.6.1: Regular detection and monitoring of unauthorized changes to payment pages. Implementation includes:

- Automated change detection mechanisms

- Alert procedures for unauthorized modifications

- Regular validation that detection systems work correctly

These requirements address “e-skimming attacks” where criminals inject malicious JavaScript into payment pages to steal card data as customers enter it.

Tokenization and Encryption

Modern e-commerce platforms should implement:

Tokenization: Replacing sensitive card data with non-sensitive tokens that have no exploitable value. The actual card data resides in a secure vault, never touching the merchant’s systems.

End-to-End Encryption: Encrypting cardholder data from the point of capture through the entire payment flow, ensuring it remains unreadable even if intercepted.

TLS/SSL Certificates: Using HTTPS with strong encryption for all e-commerce pages, especially payment interfaces.

According to RSI Security’s PCI guide:

“achieving PCI compliance involves implementing and annually reporting on precise cybersecurity measures designed to safeguard cardholder data.”

Source: PCI DSS 4.0 Compliance

Consumer Rights and Legal Remedies

E-commerce cybersecurity laws establish comprehensive consumer rights:

Right to Security

Consumers have the right to expect reasonable security measures protecting their personal and financial data. Businesses must implement industry-standard protections including encryption, access controls, and monitoring.

Right to Notification

When breaches occur, consumers have the right to prompt notification. GDPR requires notification within 72 hours, while various U.S. state laws impose similar timeframes. Notifications must explain:

- Nature of the breach and data affected

- Potential consequences

- Measures taken to address the breach

- Steps consumers can take to protect themselves

Right to Access and Deletion

Under GDPR, CCPA, and similar laws, consumers can:

- Request copies of all personal data companies hold about them

- Demand correction of inaccurate information

- Request deletion of their data (subject to certain exceptions)

- Object to certain processing activities

- Receive data in portable formats

Right to Compensation

When businesses fail to protect data adequately, consumers may seek compensation through:

- Private lawsuits for damages resulting from breaches

- Class action lawsuits for widespread harm

- Regulatory complaints triggering investigations and fines

- Chargeback rights for unauthorized payment transactions

Payment Dispute Rights

PSD2 and similar regulations establish clear liability frameworks:

- Consumers liable for maximum €50 for lost/stolen payment instruments (if not grossly negligent)

- Eight-week unconditional refund right for direct debits

- Prohibition on merchants charging additional fees for specified payment methods

- Protection against unauthorized transactions

Source: European Central Bank – PSD2 Overview

Penalties for Non-Compliance

Non-compliance with e-commerce cybersecurity laws triggers severe consequences:

Regulatory Fines

- GDPR: Up to €20 million or 4% of annual global turnover, whichever is higher

- CCPA: $2,500 per violation, $7,500 for intentional violations

- PCI DSS: $5,000 to $100,000 monthly until compliance is restored

- India DPDP Act: Up to INR 250 crores ($30 million+)

- Singapore PDPA: Up to SGD 1 million

ValueMentor reports that:

“PCI DSS violations can cost between USD 5,000 and 100,000 per month until compliance is restored, while the average cost of a data breach in the financial sector reached USD 5.9 million in 2024.”

Operational Consequences

- Suspension of payment processing capabilities

- Increased transaction fees from payment processors

- Mandatory third-party security audits at business expense

- Enhanced reporting and monitoring requirements

- Restrictions on data processing activities

Legal Liabilities

- Class action lawsuits from affected customers

- Regulatory investigations and enforcement actions

- Contractual breach claims from business partners

- Shareholder derivative actions

- Personal liability for officers and directors

Reputational Harm

According to ComplianceHub’s analysis:

“brand trust is the cornerstone of every successful digital business, and a single data breach can shatter that trust overnight, leading to mass customer attrition.”

Source: ValueMentor – PCI DSS Compliance Guide

Building a Compliance Framework

Effective e-commerce compliance requires systematic implementation:

Conduct Data Audit

- Identify all personal and payment data collected

- Map data flows through systems and third parties

- Document data retention periods

- Classify data by sensitivity level

Implement Technical Controls

- Deploy encryption for data at rest and in transit

- Enable multi-factor authentication for administrative access

- Install web application firewalls and intrusion detection

- Implement logging and monitoring systems

- Conduct regular vulnerability scans and penetration tests

Establish Policies and Procedures

- Create comprehensive privacy policies

- Develop data breach response plans

- Implement change management procedures

- Establish vendor management programs

- Document compliance processes

Train Employees

Training should cover:

- Recognizing phishing and social engineering

- Secure data handling procedures

- Incident reporting protocols

- Privacy law requirements

- Payment security best practices

Engage Third-Party Experts

Consider professional assistance for:

- PCI DSS compliance assessments and certification

- Data protection impact assessments

- Penetration testing and security audits

- Legal compliance reviews

- Incident response planning

Future of Online Retail Compliance

Several trends will shape e-commerce compliance:

AI and Automation

Artificial intelligence will increasingly automate compliance monitoring, threat detection, and response, while also introducing new risks requiring regulatory attention.

Unified Global Standards

International cooperation may lead to more harmonized standards, though regional differences will persist. The evolution from PSD2 to PSD3 demonstrates ongoing regulatory modernization.

Enhanced Authentication

Biometric authentication, behavioral analytics, and continuous authentication will supplement or replace traditional passwords, improving both security and user experience.

Privacy-Enhancing Technologies

Techniques like differential privacy, homomorphic encryption, and secure multi-party computation will enable data analysis while protecting individual privacy.

Expanded Scope

Regulations will increasingly cover emerging payment methods including cryptocurrencies, Buy Now Pay Later services, and digital wallets, as demonstrated by PSD3’s broader scope.

Conclusion

E-commerce cybersecurity compliance represents a critical business imperative in 2025, with regulations expanding globally and penalties reaching unprecedented levels. Businesses must navigate complex requirements spanning payment security (PCI DSS), data privacy (GDPR, CCPA, DPDP), and payment services (PSD2/PSD3).

Success requires systematic implementation of technical controls, organizational policies, employee training, and continuous monitoring. While compliance demands significant investment, the costs of non-compliance fines reaching millions, payment processing suspension, and reputation damage far exceed compliance costs.

Forward-thinking businesses view compliance not as a burden but as a competitive advantage, demonstrating to customers their commitment to data protection and security. By implementing robust compliance frameworks today, e-commerce businesses position themselves for sustainable growth in an increasingly regulated digital marketplace.

Glossary

Cardholder Data (CHD): Primary account number plus any combination of cardholder name, expiration date, or service code

Data Controller: Entity determining purposes and means of personal data processing

Data Processor: Entity processing personal data on behalf of the controller

Payment Service Provider (PSP): Entity providing payment services to merchants or consumers

Strong Customer Authentication (SCA): Authentication based on two or more independent elements from knowledge, possession, and inherence categories

Tokenization: Replacing sensitive data with non-sensitive tokens that have no exploitable value

Frequently Asked Questions

Do small e-commerce businesses need PCI DSS compliance?

Yes, any business that stores, processes, or transmits credit card information must comply with PCI DSS regardless of size. The validation level depends on transaction volume, but all merchants must meet the requirements.

How does GDPR apply to non-EU businesses?

Can we outsource PCI compliance to payment processors?

While using third-party payment processors reduces PCI scope, merchants remain responsible for compliance in areas they control, including website security and customer data protection.

When does PSD3 become mandatory?

PSD3 is expected to be adopted in 2025 with implementation between 2026-2027 after an 18-month transition period. Businesses should begin preparing now for the expanded requirements.