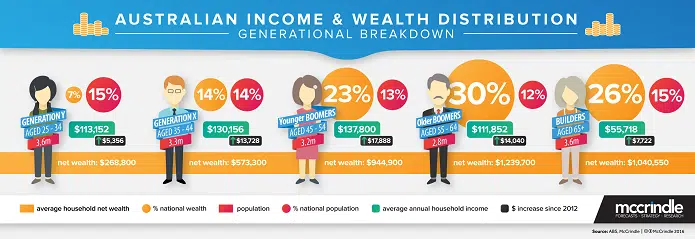

New data shows Australia’s aging population now holds more wealth than ever before, driven by rising property values and strong superannuation returns.

Australians are retiring with record levels of wealth, largely concentrated in housing, investment properties, and superannuation. This financial security helps retirees draw consistent incomes to support their retirement lifestyles.

Government Spending on Seniors Continues to Rise

Despite rising personal wealth, government spending on social safety nets for older Australians has increased in real per-person terms. This suggests that public support remains a key component in securing retirees’ wellbeing.

Research shows that earnings have increased at every stage of life, with peak incomes still occurring in people’s 50s. Moreover, retirees today benefit from higher passive income than previous generations, reflecting improved financial resilience.

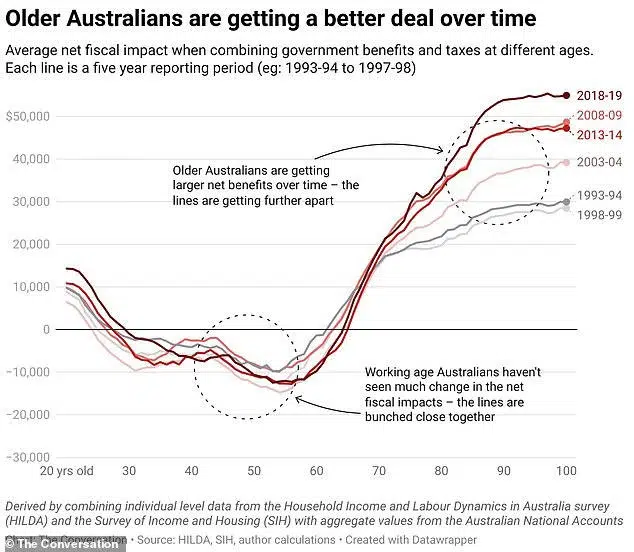

Evolution of the Tax and Transfer System

In the past, older Australians earned modest incomes and relied heavily on pensions and government support to maintain an income comparable to younger workers starting their careers.

Today’s average Australian in their 60s enjoys significantly higher private income along with increased government transfers, resulting in a post-tax income similar to that of a typical 40-year-old, but without saving or family financial pressures.

This shift represents a fundamental change in Australia’s tax and transfer system. While most government support remains means-tested, many benefits for older Australians are now age-based, reflecting the fact that age is no longer a reliable indicator of economic disadvantage.

Government Expenditure Shifts and Generational Impact

Statistics reveal that government spending on older Australians has grown substantially, funded largely by the working-age population. Simultaneously, seniors’ wealth and incomes have increased faster than other age groups.

This trend is partly driven by policies that have successfully boosted retirement incomes and wellbeing compared to decades ago. Nonetheless, these positive outcomes raise concerns about the long-term sustainability of the federal budget and call for tax system reform.

Currently, about one-third of income in Australia is untaxed. A dual income tax applying a low, uniform rate to all asset income could help address this imbalance.

Balancing Wealth Distribution Over a Lifetime

Governments attempt to smooth income across the life cycle. However, younger Australians face substantial financial challenges such as housing affordability, family expenses, and compulsory superannuation contributions of 12.5%.

Older Australians, by contrast, often maintain similar income levels without these burdens and frequently pass away with significant superannuation balances.

This dynamic results in a transfer of resources from younger Australians at their greatest need to older Australians when their needs typically diminish. Sensible reforms are needed to encourage retirement income spending and provide safeguards against financial hardship, preserving the successes of current policies while ensuring fairness for future generations.

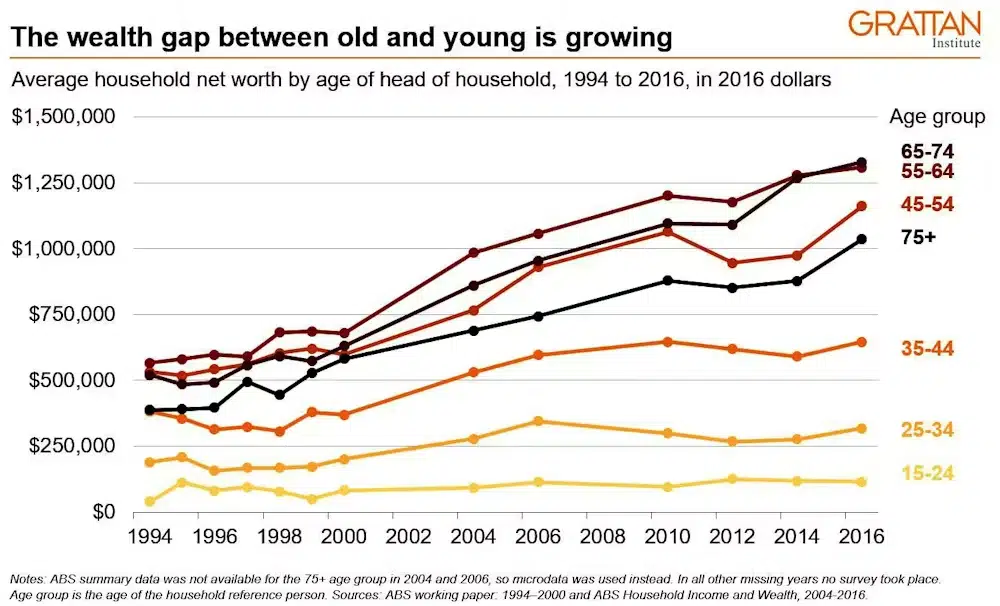

Housing Wealth Fuels Generational Inequality

House price increases over recent decades have significantly increased the wealth of older Australians, boosting private income through capital gains and imputed rent, the hypothetical rental value homeowners avoid paying.

This gain comes at the expense of younger Australians and migrants trying to enter the housing market, effectively delaying their ability to build wealth through homeownership. Those supported by asset-rich parents benefit substantially, while others may face lifelong exclusion from homeownership.

The fundamental inequality lies between young people who will inherit assets and those who will not, a gap heavily influenced by government policy.

Policy Drivers of Housing Market Distortions

Government policies that preferentially tax housing increase demand and push up prices. Zoning and planning regulations account for about 40% of housing costs in Sydney and Melbourne, and approximately 25% of land within 10 kilometers of Sydney’s CBD is protected under heritage laws.

Additional policies discourage downsizing among older homeowners. These include capital gains exemptions for primary residences, means test exemptions for owner-occupied housing, subsidies for rates and utilities, aging-in-place initiatives, and the absence of broad-based property taxes or reform of stamp duty.

Bottom Line

Australia’s aging population is wealthier than ever, yet government spending on age-related benefits keeps increasing. This growing imbalance highlights how rising private wealth hasn’t eased public dependence, putting more financial pressure on younger Australians and raising concerns about the long-term sustainability of the nation’s retirement system.